Mega Backdoor Roth

A powerful strategy for high-income earners to maximize tax-free retirement savings.

Section Guide

Introduction

High income earners often face limitations when it comes to saving more in tax-advantaged retirement accounts - especially Roth IRAs, which have strict contribution and income limits. The Mega Backdoor Roth strategy offers a powerful workaround by leveraging after-tax 401(k) contributions and in-plan Roth conversions to unlock significantly more tax-free savings.

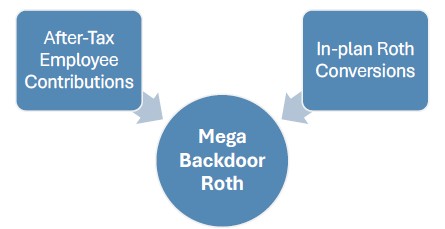

What Is a Mega Backdoor Roth?

A Mega Backdoor Roth is a savings strategy utilized in 401(k) and 403(b) plans to assist high-income earners in maximizing their retirement savings through contributing much larger contributions than the annual elective deferral limits. Depending on the plan rules, a participant is allowed to save after-tax contributions in addition to their maximized pre-tax deferrals.

Once funded, the contribution is immediately converted into a Roth via an in-plan Roth Conversion. This is a method to save more tax-free, as the standard Roth IRA has both income limits and contribution limits.

Funds invested in a Roth account grow tax-free and can be withdrawn tax-free in retirement (after age 59 ½).

Background

The IRS Notice 2014-54 clarified that after-tax contributions in a 401(k) and 403(b) plan can be split between a Traditional IRA and a Roth IRA when distributed.

Effectively, this allows in-plan Roth conversions or direct rollovers of after-tax contributions as participants can roll over the after-tax portion to a Roth IRA and the pre-tax portion to a Traditional IRA.

Types of Retirement Contributions

| Pre-Tax | Roth | After-Tax | Employer Contributions |

|---|---|---|---|

|

|

|

|

How It Works

The maximum pre-tax or Roth deferral for a participant (employee) in 2026 is $24,500 (if under age 50).

Anyone who is age 50 or older qualifies for an $8,000 catch-up contribution, bringing their maximum to $32,500.

In 2026, the 401(k) total annual additions limit is $72,000 (if under age 50) or $80,000 (for those age 50 or older).

This total includes all pre-tax, Roth, after-tax, and employer contributions.

| Category | 2026 Limit |

|---|---|

| Employee Deferral (Under 50) | $24,500 |

| Employee Deferral (50+) | $32,500 |

| Total Annual Additions (Under 50) | $72,000 |

| Total Annual Additions (50+) | $80,000 |

Example

Jim is 45 years old, single, makes $200,000 per year and has maxed out his pre-tax deferrals at $24,500 this year.

His employer matches 3% annually, meaning they contribute $6,000. In total, $30,500 has gone into Jim's 401(k) of the $72,000 allowed.

He now has the flexibility to fund an additional $41,500 into his 401(k) – but how can he do that if he already maxed out his pre-tax deferral?

This is where the Mega Backdoor Roth comes in.

Jim can contribute $41,500 more in after-tax contributions to his 401(k) and immediately perform a Roth conversion. This leaves him with $41,500 in his Roth bucket to grow tax-free.

Eligibility

Your plan must allow two key components to utilize this strategy:

To confirm eligibility, you can either review your plan’s Summary Plan Description or contact your retirement plan sponsor to verify that both after-tax employee contributions and in-plan Roth Conversions are allowed.

Strategy Steps

- Max out your pre-tax 401(k) salary deferrals.

- Confirm your plan allows Mega Backdoor Roth.

- Make additional after-tax contributions.

- Convert immediately into Roth.

Please note, changes in tax law may occur at any time and could have a substantial impact upon each person’s situation. While we are familiar with the tax provisions of the issues presented herein, as Financial Advisors of RJFS, we are not qualified to render advice on tax or legal matters. You should discuss tax or legal matters with the appropriate professional. This case study is for illustrative purposes only. Individual cases will vary. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Prior to making any investment decision, you should consult with your financial advisor about your individual situation.